Key takeaways include:

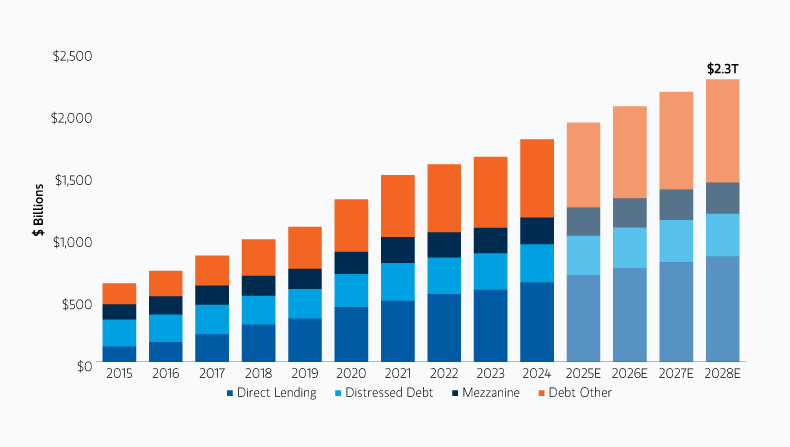

- Direct Lending is by far the single largest strategy within private credit today, having grown from 9% to 36% of total assets under management over the last 15 years.1

- This growth has been fueled by borrower need and investor demand. Middle market companies have flocked to direct lenders as the number of banks has fallen by 53%,2 and investors have seen Sharpe ratios enhanced by allocating more of their portfolios to Direct lending.

- Direct Lending’s main target market, the middle market borrower, has demonstrated lower default rates and loss ratios when compared to the large corporate market for syndicated loans, based on 25 years of historic data.3

Direct Lending is a type of Private Credit strategy that makes direct, illiquid loans to middle market companies outside of the traditional banking system. Direct Lending usually refers to first lien loans as well as unitranche loans that combine different debt classes or liens into a single loan.

Projected and historic growth in private assets

Projected and historic growth in private assets

DISPLAY 1

The middle market represents a significant cross-section of the US economy, accounting for one-third of private sector GDP, $13 trillion in revenue and 50 million workers employed.4 Despite this, banks have largely withdrawn from the middle market as they have grown larger via consolidation and more constrained with their lending due to the flood of regulations post the Great Financial Crisis.

Other growth drivers for the industry include the $1.7 trillion of dry powder that the Private Equity industry has amassed while awaiting a better dealmaking environment.5 Direct Lending has a strong presence in the leveraged buyout loan market with its share rising to as high as 93% in 2023.6 In addition, nearly $1 trillion in middle market loans are scheduled to come due by 2030, which can drive significant refinancing activity for direct lenders.7

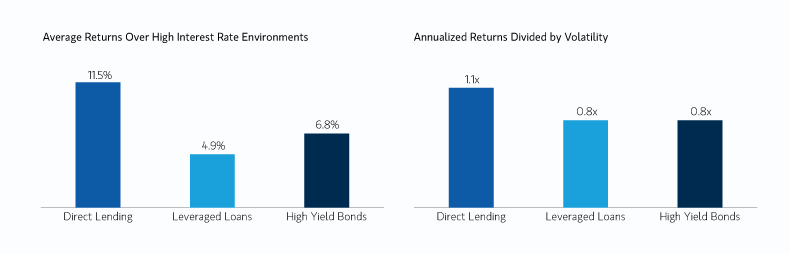

Investor demand for Direct Lending funds remains strong, underpinned by a higher-for-longer interest rate environment. Direct Lending funds have generated superior performance relative to both high-yield bonds and syndicated loans during seven periods of rising rates since 2009.8 Annualized returns divided by volatility, or Sharpe ratio, was also superior for Direct Lending relative to these two asset classes.9 This has not been lost on investors. Surveyed investors have cited Private Debt most frequently as the private asset class they intend to allocate more to.

Direct Lending, Leveraged Loans, High Yield Bond Return Comparisons

Direct Lending, Leveraged Loans, High Yield Bond Return Comparisons

DISPLAY 2

Learn more about the rise of direct lending from its small, early origins to its present role as a mainstay of the private credit industry.

Featured Insights