The market for equity mutual funds has been fundamentally reshaped by passively managed funds: Last year, for the first time since their introduction in the 1970s, passive equity fund assets surged past the $12.2 trillion in active funds, according to Morningstar, as of December 31, 2023. Unsurprisingly, passive fixed income investing has also gained in popularity in recent years.

Is the popularity justified? Based on a decade's worth of performance reviewed in a new Eaton Vance study,1 the answer is no.

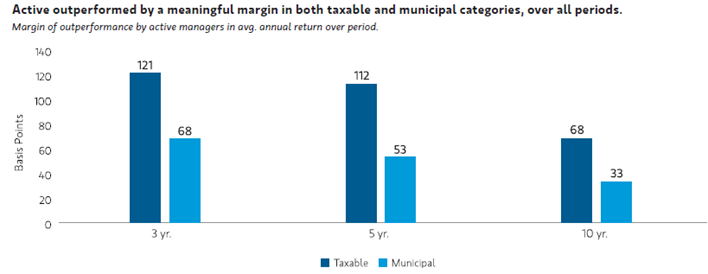

The analysis shows that active fixed income managers have handily outpaced the passive ones, based on a review of 327 funds with $2.2 trillion in assets across nine major fixed income Morningstar categories. The summary chart below highlights that active outperformed by a meaningful margin over all periods studied, on both sides of the taxable/tax-exempt divide, particularly during the past three years—a period scarred by the massive bond market sell-off of 2022. This highlights the ability of active managers to capture return potential for investors while mitigating downside risk.

Source: Eaton Vance research based on Morningstar U.S. fund data and categories, as of December 31, 2023. See footnote 1 for description of methodology. Past performance is no guarantee of future results.

Additional highlights of the study include:

- Actively managed funds in nine major Morningstar fixed-income sectors beat passive funds over the 3-, 5- and 10-year investment horizons studied.

- Active managers maintained marked consistency in their outperformance: They prevailed over passive funds in all rolling three-year periods over the decade analyzed, with a winning batting average of 87% across the nine categories.

- Explanations for the consistent underperformance by passive funds may include their lack of flexibility to adapt to changing market conditions, self-limiting opportunity sets and other factors.

- Active managers have discretion to take action that seeks to improve returns, enhance yield or lower risk, and the analysis of the historical record suggests that, on balance, they have used that discretion effectively.

Bottom line: Performance-focused bond investors should look beyond the superficial appeal of passive funds and consider where the superior returns have actually been delivered.

To read the full research report, click here.

1Source: Eaton Vance research based on Morningstar U.S. fund data, comparing actively managed fund net returns with passive funds, based on the lowest expense ratio share class performance on an equal weighted basis, as of December 31, 2023. Active management attempts to outperform a passive benchmark through proactive security selection and assumes considerable risk should managers incorrectly anticipate changing conditions. The study considered a Morningstar universe comprising 793 active funds with $1,438 billion in assets under management (AUM) and 137 passive funds, with $1,097 billion AUM, including both open end funds and ETFs, in nine well-defined and relatively homogeneous fixed income categories. We made several adjustments to ensure balanced and fair comparisons, starting with analysis of the benchmarks used by all funds—active and passive—within a certain category. We then excluded funds benchmarked to indexes that don't represent the general characteristics of the category. This included indexes that generally did not match the category's overall characteristics based on criteria such as credit, duration, geographic or asset class. We further applied an AUM floor of $500 million (as of 1/31/2024). After applying the benchmark and AUM filters, the study's universe included 289 active funds with $1,226 billion AUM, or 85% of the original, and 38 passive funds with $982 billion AUM, or 90% of the original. Past performance is no guarantee of future results.

Featured Insights

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. The indexes are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto.