The Magnificent 7's (Mag 7) market dominance and chart-topping performance have captured headlines in recent years. Small caps, by contrast, have lagged in performance and market attention. Nonetheless, there is a strong case to be made for investing in quality small caps today.

Anyone with even a passing interest in the equity market over the last few years is likely familiar with the Mag 7—those select, and undoubtdedly impressive, household names that have driven a significant portion of the S&P 500's performance—and now represent a large percentage of that benchmark.

The Mag 7 are emblematic of a broader trend of rising market concentration, a dynamic seen several times throughout market history, as others, such as Mauboussin and Callahan of Morgan Stanley Investment Management, have observed.1

A decade of large-cap concentration

2014 marked the beginning of this most recent period of rising market concentration that has seen a handful of large-cap winners dominating equity returns. Over this decade-plus run, this upper echelon of market darlings has also accounted for a meaningful portion of total economic value creation, while generating enviable free cash flow, growth and returns on invested capital.2 In other words, they've earned it!

When coupled with the prolonged underperformance of small-cap stocks over this same timeframe, perhaps justified by their inferior return on invested capital (ROIC) characteristics compared to their large-cap peers, many have concluded that the small-cap universe has little to offer. Herein lies the myth.

Quality small caps outperform

The small-cap universe, as measured by the Russell 2000®, offers significant opportunities for capital appreciation when approached with a quality lens, even in a period characterized by large-cap dominance and increased market concentration. We believe a high-quality, actively managed small-cap allocation can still offer attractive risk-adjusted returns in a well-diversified portfolio that includes large-cap holdings.

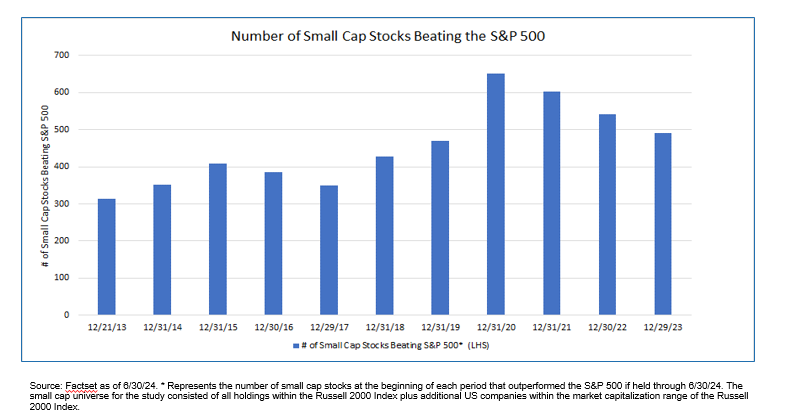

Since 2014, despite the dominance of the Mag 7, there are literally hundreds of small-cap stocks one could have purchased at the start of each year and, if held, would have outperformed the cumulative return of the S&P 500 (through 6/30/24).

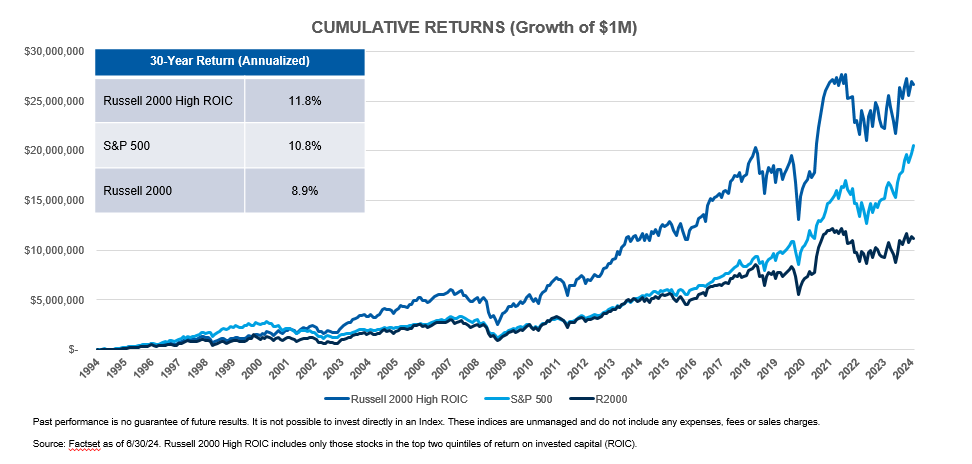

In our view, one of the best measures for identifying quality in this small-cap opportunity set is ROIC. Looking back over the 20 years preceding this current period of market concentration, a high-quality, small-cap allocation, as measured by ROIC, has produced returns that are competitive with, and frequently surpass, large-cap equities.

Bottom line: We do not know if we're nearing the end of rising large-cap market concentration. But we do know that an active, quality-focused approach to small-cap investing is worth considering for a portfolio allocation, regardless of whether the Mag 7's days of dominance are numbered, or not.

1. Morgan Stanley, Consilient Observer, June 4, 2024, "Stock Market Concentration: How Much is Too Much?" by Michael J. Mauboussin and Dan Callahan, CFA.

2. Ibid.

S&P 500 is a stock market-capitalization weighted index tracking the stock performance of 500 of the largest U.S. companies.

Russell 2000® Indexis an unmanaged index of 2,000 U.S. small-cap stocks. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of any investment.

Risk Considerations: The value of investments may increase or decrease in response to economic and financial events (whether real, expected or perceived) in the U.S. and global markets. The value of equity securities is sensitive to stock market volatility. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, more established companies.

Featured Insights

Risk Considerations: The value of investments may increase or decrease in response to economic and financial events (whether real, expected or perceived) in the U.S. and global markets. The value of equity securities is sensitive to stock market volatility. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, more established companies.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. The indexes are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto.