KEY POINTS

1. Ireland, one of Europe's fastest-growing economies, has experienced strong economic growth over the past decade.

2. We believe Ireland is on the cusp of a new credit cycle driven by rising household income outpacing household debt.

3. Attractive valuations and durable earnings power, driven by strong loan growth, is fueling investment opportunities in the Irish banking sector.

One of Europe's fastest growing economies, Ireland has a small but mighty banking sector which helps to nourish the country's economic landscape. After crumbling in 2007, Irish banks embarked on a fierce climb, hitting a peak of €770.44 billion in the third quarter of 2022.1 Despite periods of fluctuation, the banking sector has grown significantly over the last decade, from €502.81 billion in the fourth quarter of 2014 to €716.09 billion in the fourth quarter of 2023. As household income outpaces household debt, we believe Ireland is poised for a new credit cycle that will boost the banking sector.

Supportive demographic trends

With a population of just over five million people, about the same as the U.S. state of Alabama, Ireland's nominal gross national income (GNI) growth has averaged over 7% annually over the last decade.2 This flourish is supported by demographic trends, such as supportive immigration policies, which have helped to increase Ireland's working age population by over 9% since 2013. Over the next decade, Ireland's working age population growth rate is projected to be nearly double that of the UK.3 Moreover, improvements in productivity have led to per capita income growth of over 6% per year.4

The Emerald Isle's economic story wasn't always so rosy. Once recognized as one of Europe's poorest countries, Ireland's growth accelerated after it implemented pro-business reforms and favorable corporate tax laws to draw in foreign direct investment.

The upward momentum came to a halt in 2007 with the onset of the global financial crisis (GFC). The banking sector collapsed, hurt by excessive leverage, poor underwriting and a housing market crash, and had to be bailed out by the Irish government with the aid of the International Monetary Fund (IMF). The government shut down poorly run banks while merging and recapitalizing viable players. New regulations were also introduced to help protect against a similar failure.

Housing outlook a key factor

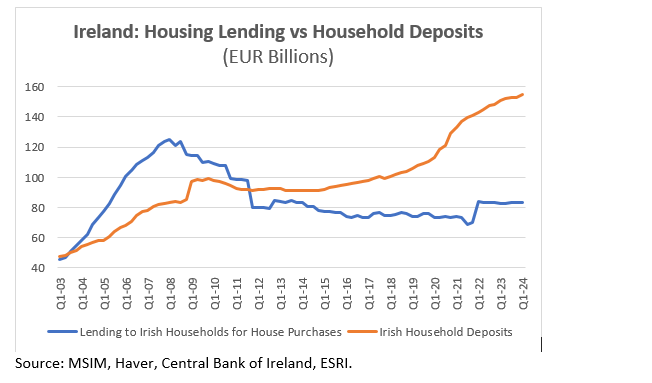

Today, Ireland's banks are less leveraged, better capitalized and boasting far more deposits than loans, a stark contrast to the years before the GFC. Foreign banks, faced with increased regulatory requirements and industry consolidation, have effectively exited the country. The sector today resembles a domestic duopoly, where the top two players hold three-quarters of household deposits.

While Irish bank shares have substantially rebounded from pandemic lows, the entire sector remains below book value.5 Why? Concerns loom over a potential macroeconomic downturn impacting house prices and credit quality, coupled with fears of declines in net interest income (NII) once the European Central Bank (ECB) implements rate cuts.

Though credit quality concerns are valid, we see less likelihood of a severe housing market correction. This is an important angle to examine because residential mortgages account for a sizable chunk of the banking sector's loan book. In the years leading up to the GFC, the housing stock grew faster than the population, fueled by speculative demand. Since then, housing supply has lagged population growth, suggesting current price levels are driven by fundamental supply-and-demand dynamics rather than speculation.

Some investors are concerned that ECB rate cuts will cause material NII declines in the near term. While we appreciate that the banking sector has parked large quantities of excess deposits with the central bank, we believe there is long-term profitable loan growth potential for Ireland. A stronger-than-expected loan demand could offset the rate cut headwinds.

Our analysis of credit cycles across various countries shows that after periods of deleveraging, credit growth is likely to rebound. In the period leading up to the GFC, Ireland's household debt-to-GNI ratio climbed 50 percentage points peaking in 2009 at 104%. Today it is 33%. We think this remarkable deleveraging, coupled with the country's tight housing supply, creates room for increased lending against a more fundamentally sound housing asset class. In our view, rising house price-to-income ratios and a recent relaxation in government lending regulations are a catalyst.

Bottom line: The Irish banking sector has attractive total return yields and has incrementally increased capital returns to shareholders through buybacks and dividends. These shareholder-friendly policies, coupled with cheap valuations, attractive industry dynamics, and our positive macro view are among the reasons we believe the Irish banking sector offers some of the most compelling investment opportunities in the global equities landscape today.

1 Statista.

2 GNI is an indicator designed by Ireland's Central Statistics Office to more accurately capture the domestic economy. It is calculated by removing distortions in gross domestic product (GDP) caused by foreign company operations (e.g., intellectual property purchases, aircraft leasing) which have minimal direct impact on the domestic economy.

3 Source: UN.

4 World Bank national accounts data and OECD National Accounts data files.

5 Source: Bloomberg (based on MSCI Ireland Banks constituents).

Featured Insights

Risk considerations: There is no assurance that a portfolio will achieve its investment objective. Portfolios are subject to market risk, which is the possibility that the market values of securities owned by the portfolio will decline and that the value of portfolio shares may therefore be less than what you paid for them. Market values can change daily due to economic and other events (e.g. natural disasters, health crises, terrorism, conflicts and social unrest) that affect markets, countries, companies or governments. It is difficult to predict the timing, duration, and potential adverse effects (e.g. portfolio liquidity) of events. Accordingly, you can lose money investing in this portfolio. Please be aware that this portfolio may be subject to certain additional risks. In general, equities securities' values also fluctuate in response to activities specific to a company. Investments in foreign markets entail special risks such as currency, political, economic, market and liquidity risks. The risks of investing in emerging market countries are greater than the risks generally associated with investments in foreign developed countries.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. The indexes are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto.