The impressive performance of corporate credit markets to start the year has prompted many investors to begin seeking out alternative sources of yield and total return in the global fixed income markets. One sector that has been garnering increased attention is the nearly $13 trillion global securitized market, which includes residential mortgage-backed securities (RMBS), commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS). While we believe that securitized assets broadly appear attractive today, the size of the market and the variety of unique subsectors it encompasses requires investors to be very discerning when evaluating the opportunities and risks in the sector. Below are some of our Mortgage and Securitized Team's favorite sectors, as well as those we believe warrant some caution.

Agency RMBS: Relative valuations remain compelling vs. other high-quality options

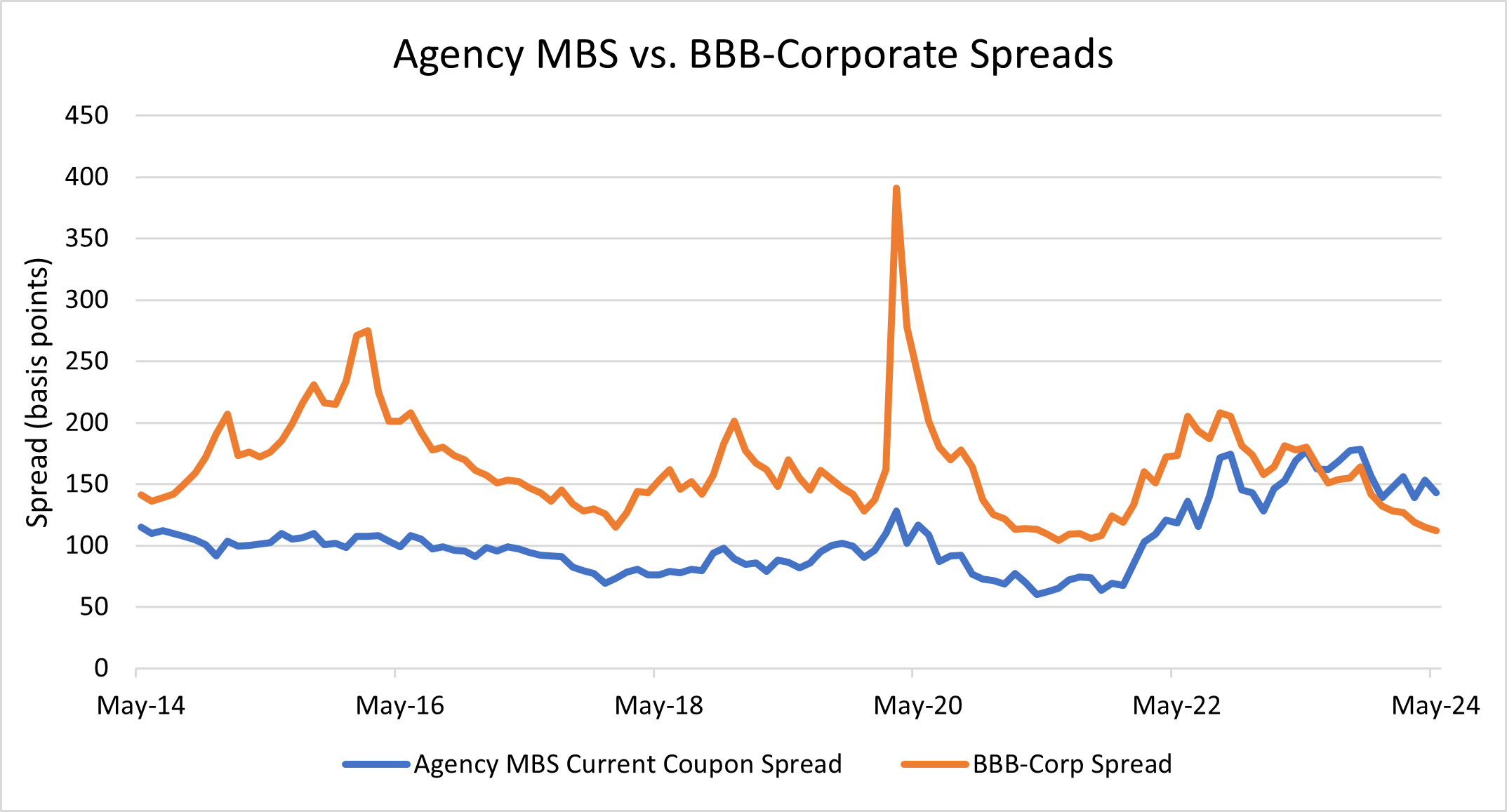

Mortgage spreads have tightened by ~40 basis points since late last year after bond markets began pricing in a less-hawkish Federal Reserve. That said, we can't forget about the 120 bps of spread widening we experienced from October 2021 through October 2023, which was driven by a combination of quantitative tightening, regional banking pressures and heightened interest rate volatility. We expect the latter two of these headwinds to subside through the end of the year, and with agency MBS spreads still trading roughly 40 basis points wider than long-term averages, the sector remains attractive.

Source: Bloomberg. As of 5/31/24. Agency MBS: Fannie Mae Current Coupon MBS Spread and BBB Corp: ICE BofA US BBB Corporate Index Spread. The index performance is provided for illustrative purposes onlyand is not meant to depict the performance of a specific investment. Past performance is no guarantee of future results.

For yield-buyers, absolute yields in the agency MBS market should be enticing, as the current coupon MBS yield is above 6% and near its highs since 2007, and relative value buyers should be even more excited, as spreads in this U.S. Government-guaranteed sector are ~30 bps wider than BBB-rated corporate bond spreads. We continue to find value in specified pools of high-coupon MBS, where we are targeting stories with a lower likelihood of refinancing, and we also think attractive opportunities exist in the CMO market, where we can find much wider spreads than in similar-duration low-coupon MBS.

Non-Agency RMBS: Strong prospects given stable housing market, strong employment and low rates on outstanding mortgages

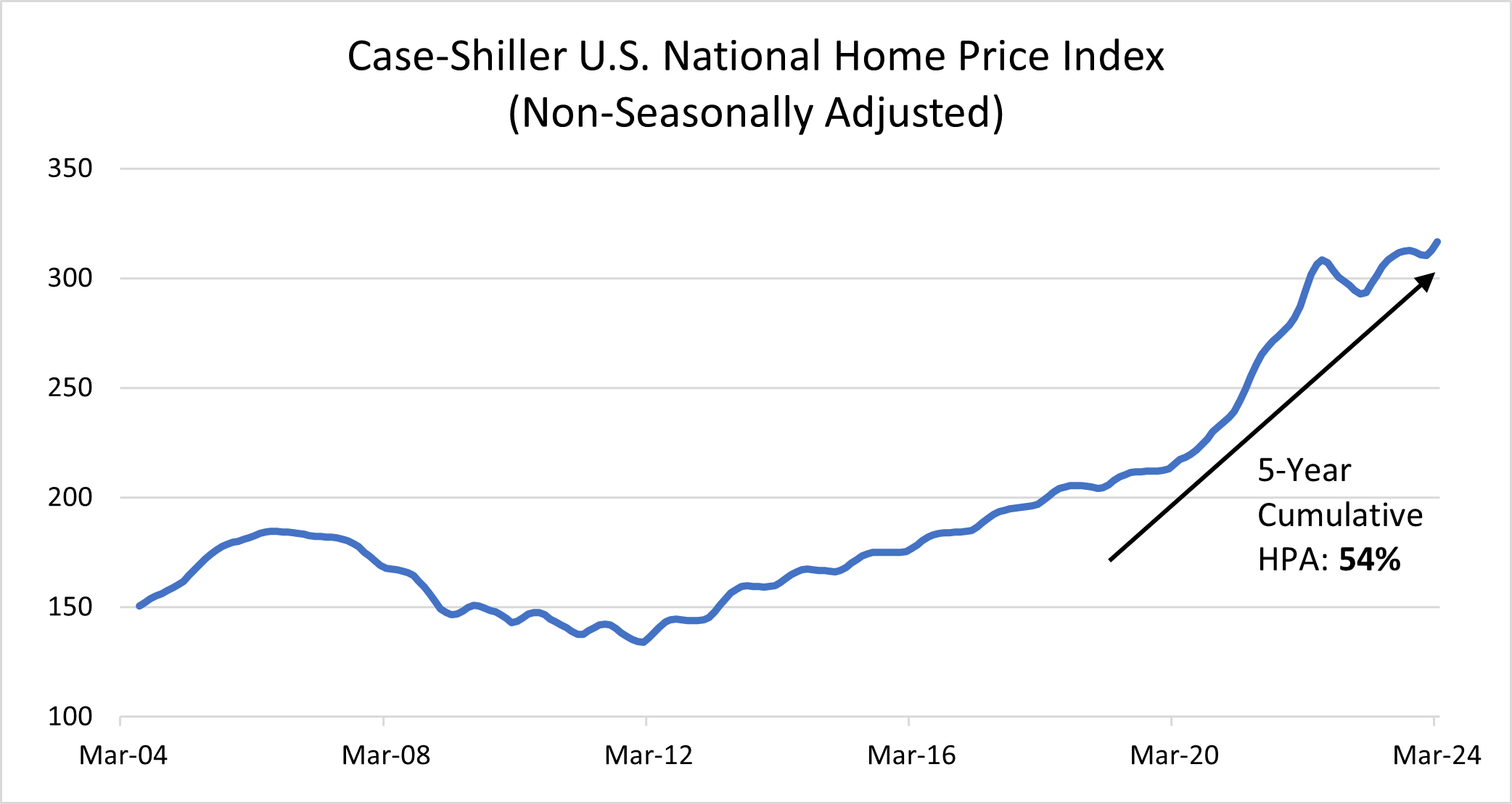

The non-agency RMBS market continues to perform well in 2024 amidst a favorable backdrop for both technicals and fundamentals. Demand remains strong and continues to outpace new issuance, while delinquencies and default rates have hovered around historic lows thanks to more conservative loan underwriting post-Financial Crisis. Home prices in the U.S. are up nearly 50% since the onset of the pandemic, yet we expect them to remain stable given the severe lack of homes available for sale.

Source: Bloomberg. As of 3/31/24.

While non-agency RMBS valuations vary widely by subsector, they remain generally attractive today, especially when considering the industry backdrop. Absent a steep decline in mortgage rates, new origination should remain light due to challenging home affordability, and this supports market technicals. Meanwhile, stable household balance sheets and a strong employment market each support borrower credit. The combination of strong fundamentals and favorable technicals is positive for residential credit.

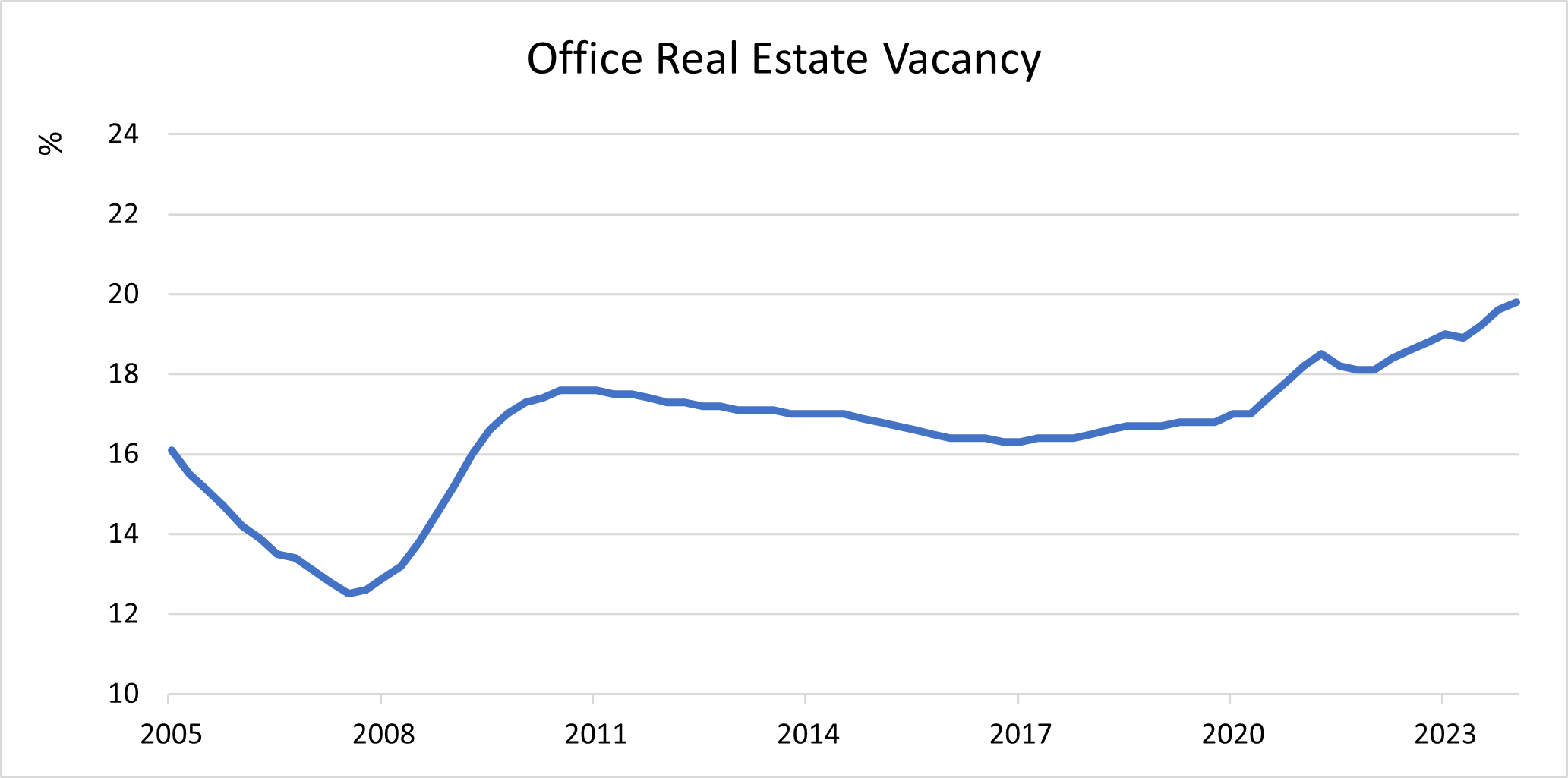

CMBS: Rent growth has peaked and higher financing costs are stressing commercial real estate

Like many other segments of the securitized market, commercial mortgage-backed securities have performed quite well this year, yet we are generally in agreement with today's negative sentiment on the sector and believe caution is warranted. The spike in rates and the resulting higher financing costs have pressured all parts of the CMBS market, but we are most wary of office CMBS. As many companies have been able to reduce their physical footprints in response to an increasingly flexible, hybrid work environment, the office sector has experienced the brunt of that negative impact in the form of rising vacancies and falling rent growth.

Source: Bloomberg. As of 3/31/24.

While risks remain in the CMBS market, there are select opportunities to take advantage of in adjacent sectors, such as the single-family rental market. Single-family rental properties have benefited from the aforementioned favorable housing market technicals, while high underlying mortgage rates have made it more affordable for many borrowers to rent rather than own, keeping vacancies low.

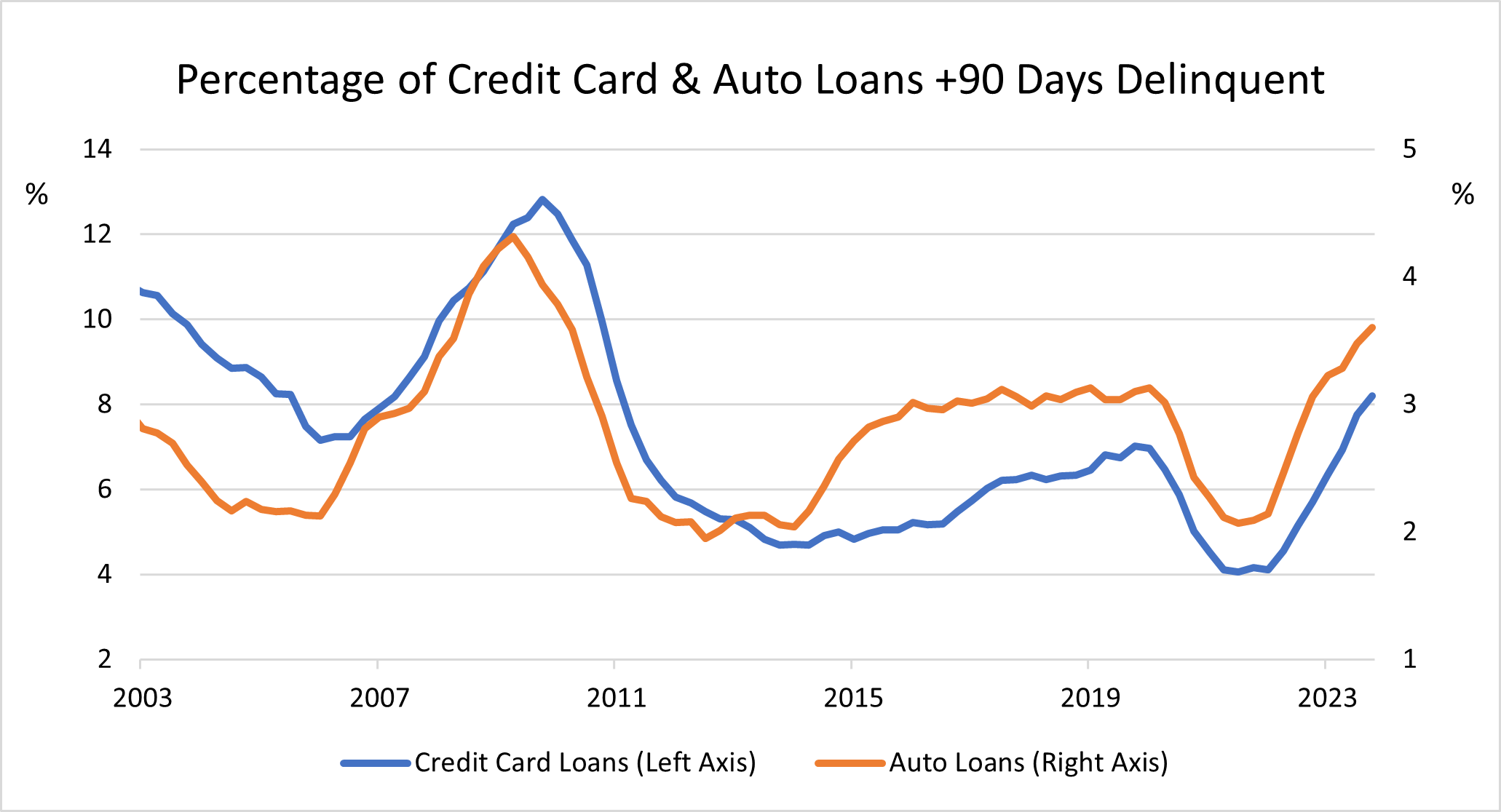

ABS: Consumer ABS appear rich, especially given expectations for a weakening consumer into year-end

The ABS market has had a similar experience as the non-agency RMBS market this year, as strong demand has more than offset an increase in supply, pushing spreads tighter. Overall, we remain cautious on consumer ABS and have instead been favoring business-oriented ABS. While household balance sheets are starting from a strong position, we expect them to weaken as pandemic-related savings have been depleted and student loan payments have resumed. This is already starting to show in the form of rising credit delinquencies, most notably among lower-income borrowers, causing us to tread carefully with regards to lower-rated consumer ABS. Instead, business-oriented ABS, which include small business loans, aircraft ABS, etc., appear much more attractive given the wider spreads offered by these securities.

Source: Macrobond. As of 2/28/24.

Source: Macrobond. As of 10/31/2023.

Bottom line: To repeat a phrase that has become increasingly popular in recent years - there is once again income in fixed income - and we would argue that the securitized markets offer some of the most attractive risk/reward opportunities in fixed income markets today.

Featured Insights

Risk Considerations: Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest-rate risk), the creditworthiness of the issuer and general market liquidity (market risk). In a rising interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining interest-rate environment, the portfolio may generate less income. Longer-term securities may be more sensitive to interest rate changes. Mortgage and asset-backed securities are sensitive to early prepayment risk and a higher risk of default and may be hard to value and difficult to sell (liquidity risk). They are also subject to credit, market and interest-rate risks.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. The indexes are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto.