KEY TAKEAWAYS

- Our strategies focus primarily on bottom-up, fundamental stock analysis. While we typically maintain diversified sector exposure, preferring stock picking over sector calls or factor tilts.

- Financials typically make up more than 20% of the value index. Within this sector, however, many of our sub-sector views are non-consensus.

- Here, we take a closer look at where we see potential opportunities and pitfalls within certain financials sub-sectors, including banks, insurance and diversified financials. Within the sector, we generally prefer non-bank companies that have the potential to compound more smoothly than the banks.

The Value Equity Team manages strategies using a fundamental, bottom-up assessment of companies. We typically maintain diversified sector exposure, preferring stock picking over sector calls or factor tilts. We strive to find unloved opportunities that our fundamental analysts believe are priced at a discount to their intrinsic value.

Within the Russell 1000 Value Index, a sizable component (typically more than 20% of the index) is financial companies. Under the financials sector hood, there are a variety of sub-sectors. Since our positioning is bottom-up, we don't maintain exposure to every sub-sector just for the sake of it. We only invest where we see a true opportunity to close the gap to a company's intrinsic value.

While our positioning is security-based, certain general themes resonate within specific sub-sectors. In financials, several of our sub-sector views are non-consensus.

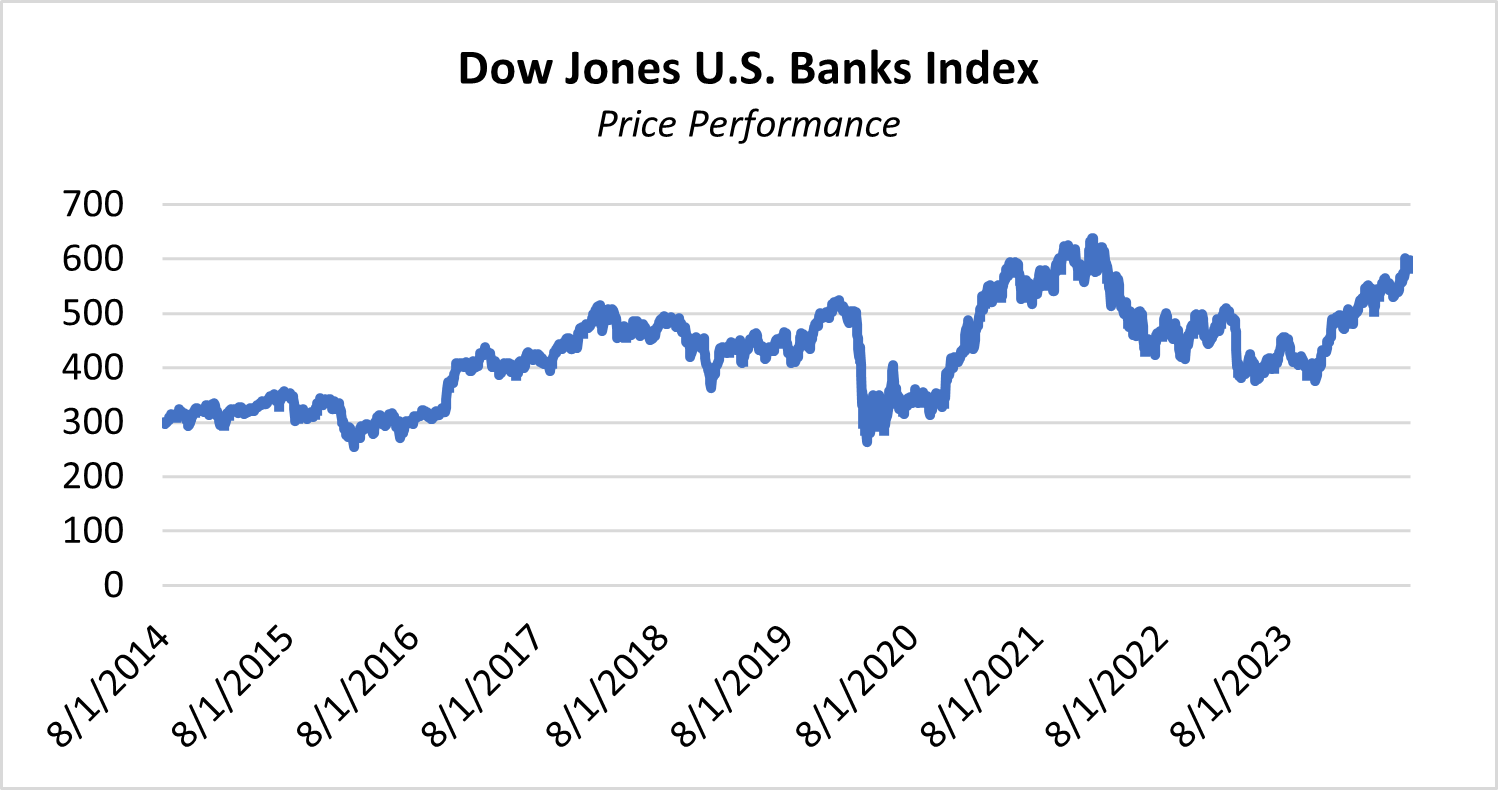

Banks

While banks are generally better capitalized today, historically their investment performance has often been uneven (see Exhibit 1). Of course, not all banks can be lumped together, and we see opportunities where some may be trading below their true intrinsic value, but selectivity is essential in identifying these.

Exhibit 1 - U.S Banks' Return Journey: +6.87% Over Recent 10 Years

Source: S&P Dow Jones. Data as of July 30, 2024. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

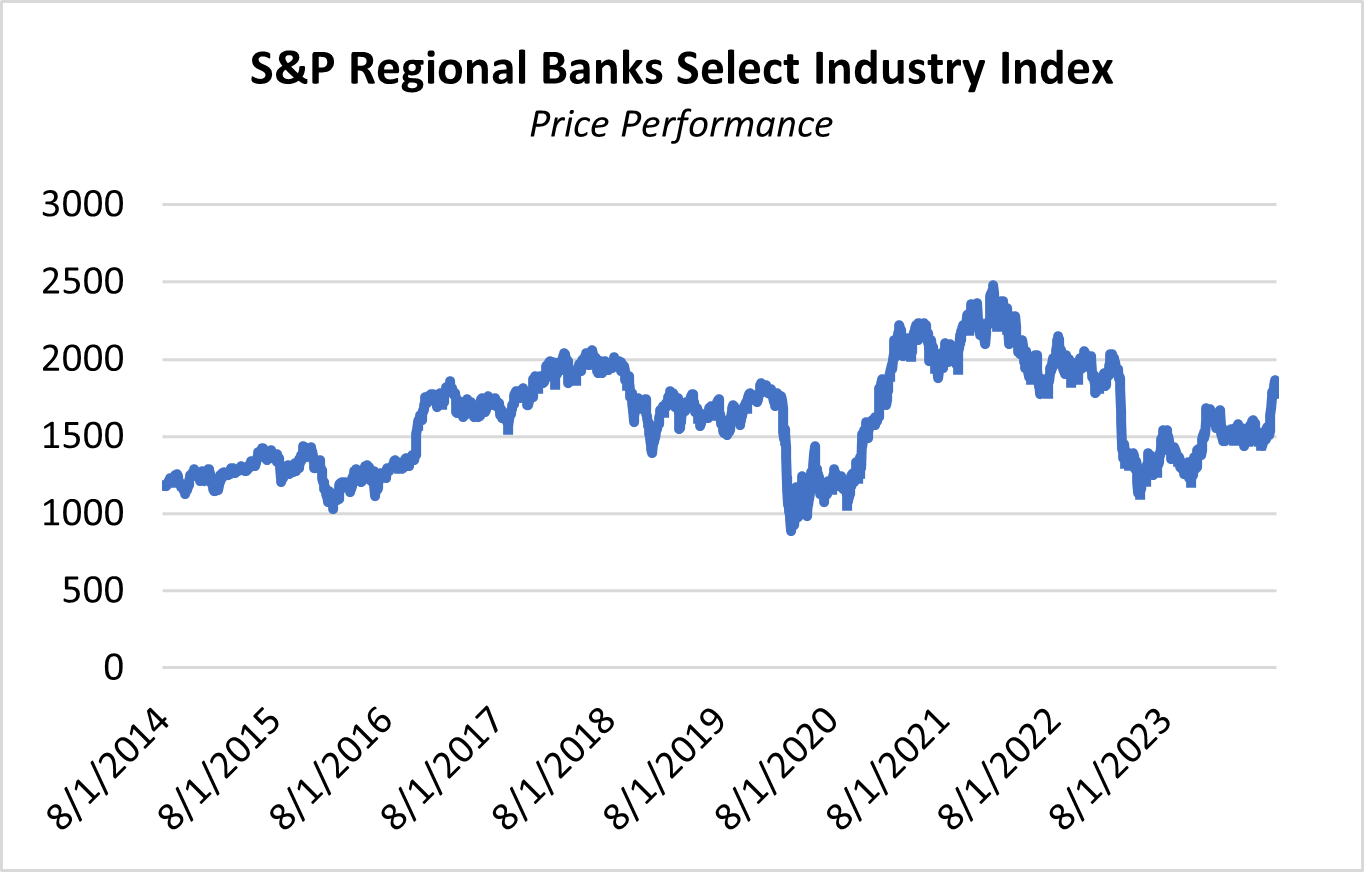

Going one layer deeper and breaking out regional banks from large national banks, we find important distinctions (Exhibit 2). Generally, most regional banks do not compound significant value over the long run. Although there are high-quality exceptions where an investment in a regional bank might be justified, those instances are typically for specific periods of time and driven by specific fundamental conditions.

Exhibit 2 - Regional Banks, Selection Matters: +4.31% Return Over 10 Years

Source: S&P Dow Jones. Data as of July 31, 2024. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

Further, the recent rise in bank stocks from late June through July 2024 largely mirrors their performance following the Trump Administration's 2016 election. We believe this possible political rotation (and the upside the Trump Administration could potentially bring - easier regulation, more possible mergers) is now largely priced into many bank stocks. However, we see more potential risks for banks now than during the 2016-2017 period. In our view, the Federal Reserve's movement on rates and the consumer's strength (or lack thereof, in both cases) present more potential wildcards than at that time. There is a risk that a negative credit cycle could still come to pass.

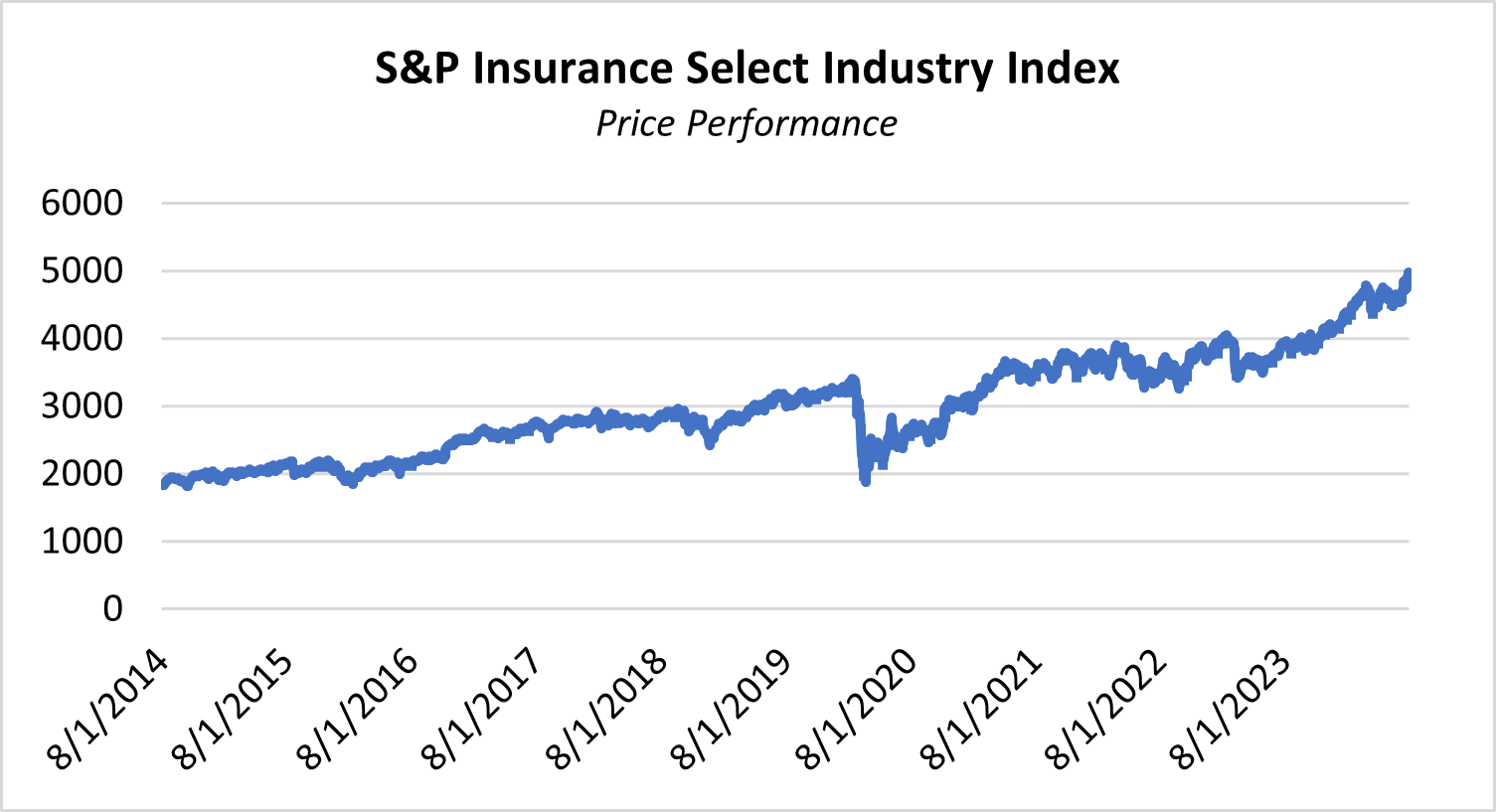

Insurance

The insurance sub-sector consists of companies with differentiated capabilities and more concentrated industry structures, leading to more accurate and constructive pricing. Over time, this allows growth to compound at a higher and steadier rate compared to other financials sub-sectors. In some cases, these qualities can lead to superior margins (Exhibit 3). Selectivity is key within this sub-sector, in finding companies that exhibit these attractive aspects of the sub-sector, and which are working to close the gaps to their intrinsic value.

Exhibit 3 - Insurance, A Potentially Smoother Ride: +10.49% Return Over 10 Years

Source: S&P Dow Jones. Data as of July 31, 2024. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

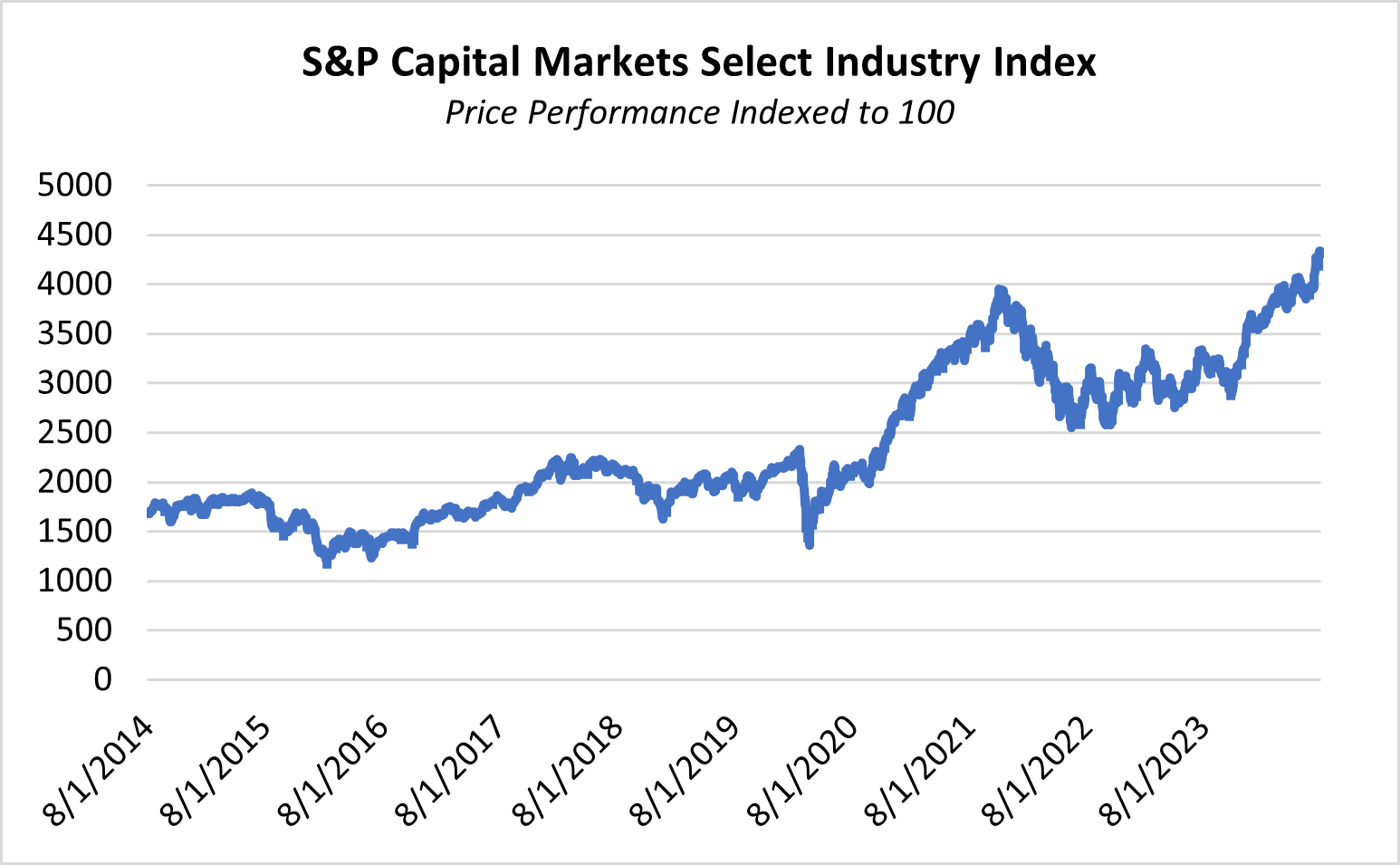

Diversified financials

This sub-sector tends to be less balance sheet/capital intensive compared to others within financials, as well as less scrutinized from a regulatory and political perspective. Given their predilection for higher growth and less risk (typically) than other financials, diversified financials tend to be higher-valued companies over time (Exhibit 4). Over the longer-term, we anticipate secular growth in wealth management both within the self-directed and independent spaces.

Exhibit 4 - Diversified Financials, Potential for Secular Growth: +9.78% Return Over 10 Years

Source: S&P Dow Jones. Data as of July 31, 2024. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

Bottom Line: Within financials, we generally prefer non-bank companies that have the potential to compound more smoothly than the banks. However, we may invest in a bank if it fits our high-quality Opportunistic Value philosophy, trades at a discount to intrinsic value, and presents a cyclical opportunity. Our strategies do not own companies simply to ensure diverse exposure; we seek to consistently ensure that capital (and accordingly, position sizing) is in those areas where we see the greatest reward- to-risk potential. Our investment team's average experience of 25 years is essential to identifying these opportunities.

Featured Insights

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Russell 1000® Value Index is an unmanaged index of U.S. large-cap value stocks. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of the fund.

Past performance is not a guarantee of future results.

Risk Considerations: The value of investments may increase or decrease in response to economic, and financial events (whether real, expected or perceived) in the U.S. and global markets. The value of equity securities is sensitive to stock market volatility. Diversification does not eliminate the risk of loss. Active management attempts to outperform a passive benchmark through proactive security selection and assumes considerable risk should managers incorrectly anticipate changing conditions.

The views and opinions and/or analysis expressed are those of the author or the investment team as of the date of preparation of this material and are subject to change at any time without notice due to market or economic conditions and may not necessarily come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing, or changes occurring, after the date of publication. The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass. Information regarding expected market returns and market outlooks is based on the research, analysis and opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to pass and are not intended to predict the future performance of any specific strategy or product the Firm offers. Future results may differ significantly depending on factors such as changes in securities or financial markets or general economic conditions.

This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and the Firm has not sought to independently verify information taken from public and third-party sources.

This material is a general communication, which is not impartial and all information provided has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Past performance is no guarantee of future results. The indexes are unmanaged and do not include any expenses, fees or sales charges. It is not possible to invest directly in an index. Any index referred to herein is the intellectual property (including registered trademarks) of the applicable licensor. Any product based on an index is in no way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with respect thereto.