KEY TAKEAWAYS

In our opinion:

- The scale of private credit—lending to companies by institutions other than banks—is not outsized when considered in the context of several factors.

- While spreads have tightened, the credit attributes of new deal activity have not changed dramatically in the past year.

- We expect deal flow will continue to increase amid generally conducive private and public financing markets, and as private equity (PE) remains poised to return investor capital.

- Direct lending—private credit extended primarily to middle market companies—remains an attractive market that has historically generated strong risk-adjusted returns.

The Growth of Private Credit—and Direct Lending—in Context

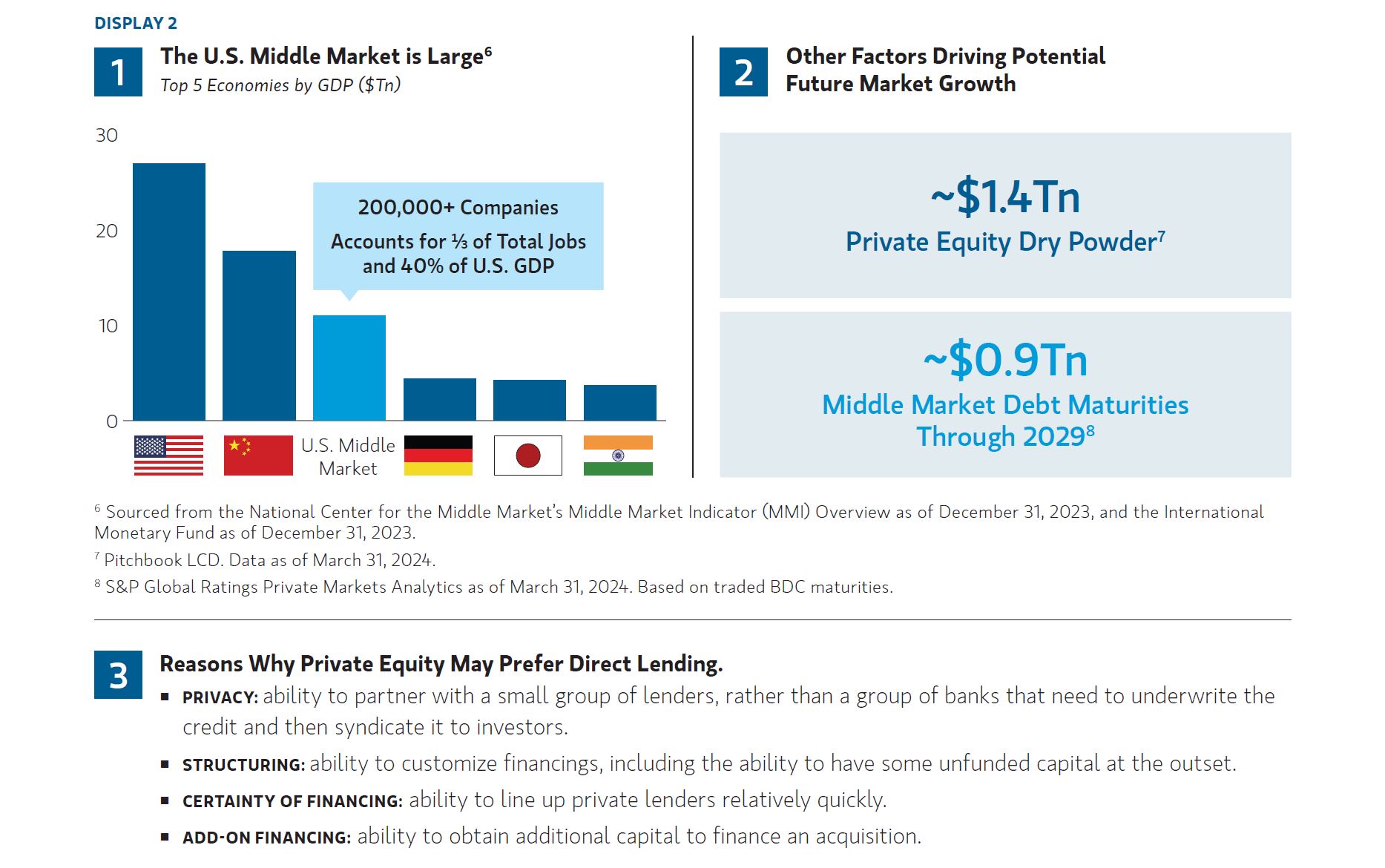

As banks have gradually retreated from middle-market lending, and public capital markets have skewed larger and exhibited volatility, private credit has stepped in to fill the void. Private credit expanded to approximately $1.5 trillion at the start of 2024, up from $1 trillion in 2020, and is estimated to reach $2.8 trillion by 2028.1

This growth has been supported by PE, which controls nearly $8 trillion in assets globally, including $4.1 trillion in the U.S.2 We believe these firms have significant dry powder to invest. All of this is relative to $20T in U.S. bank balance sheets, which have grown by around $7T in the last decade.3

We believe the direct lending market has always been competitive, and the current market is no different. The asset class has generated strong and stable returns for decades and, we believe, will continue to attract investor capital.

We believe that direct lending is positioned for continued growth for three fundamental reasons: (1) the U.S. middle market is large; (2) private equity dry powder remains at record high levels and refinancing volumes are expected to remain high; and (3) there are enduring structural benefits for borrowers.

DISPLAY 1-3

Cutting through the Noise

Despite recent press on purported lack of transparency and opaque valuation policies in the direct lending space, we believe a host of regulatory, legal, accounting and other regimes dictate that managers abide by stringent valuation policies. These policies are typically multi-layered, and they leverage both internal valuation models and third-party valuation firms to value individual loans. These valuations typically take into account fundamental company performance and market factors. Their frequency will depend on the structure of the fund in which the loans are held. For instance, some perpetually offered business development companies (“BDCs”) could be valued as frequently as monthly.

It is important to remember that in the business of making first lien loans backed by a deep base of sponsor equity, the goal is return of principal.

What We’ve Been Seeing in the Direct Lending Market

- DOCUMENTATION: While competition for deals remains fierce, we generally have witnessed documentation that remains prudent, with proper protections. Intensive credit underwriting and documentation have typically been a trademark of buy-and-hold investing in the direct lending market.

- SPREADS: Spreads on new loans have compressed over the last two years, largely in response to improving risk sentiment and a resurgence in the public capital markets; however, base rates remain elevated, generally resulting in total coupons of ~10%+.

- CREDIT QUALITY: Credit quality has not changed dramatically in the past year. We believe that the sector has performed extremely well throughout this inflationary environment, perhaps in large part due to the resilience of the underlying U.S. economy and the emerging signs that the Federal Reserve’s efforts to combat inflation has begun to work.

- DEFAULTS: Non-accruals and defaults for direct lending remain below historical averages—in the low-single digits. Should interest rates remain elevated, it is possible we would see expectations for defaults to increase gradually and trend to the historical averages. Conversely, repricing activity and lower rates would provide some relief to borrowers.

- DEAL FLOW: Sponsored middle market loan activity remained relatively resilient during the first half of 2024, partly supported by demand for incremental or add-on financings. We remain optimistic that new middle market leveraged buyout activity may accelerate with more visibility on the trajectory for interest rates. We expect deal flow to continue to accelerate into 2025, as PE remains poised to return investor capital.

Conclusion

We believe direct lending continues to offer compelling relative value compared with other assets classes and offers an attractive diversification alternative to public fixed income. And, importantly, when considered in the context of other markets, private credit has significant room to grow.7

Featured Insights